Innovation Policy Based on Canada’s Technological Specialization and Competitiveness

Disclaimer: The French version of this editorial has been auto-translated and has not been approved by the author.

Zafer Sonmez

Lead Research Associate

Conference Board of Canada

Alain Francq

Director of Innovation and Technology

Conference Board of Canada

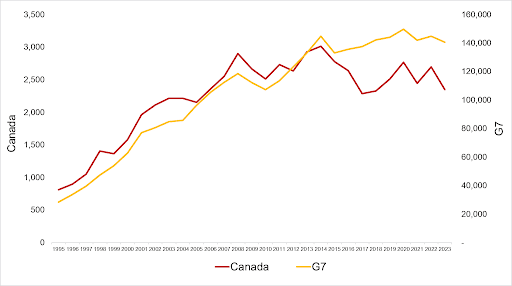

Prolonged weak business investments in machinery, equipment and intellectual property are associated with low productivity in Canada (Bank of Canada, 2024). Related to this trend is our declining competitive industrial performance (CIP). CIP was increasing in the 1990s, but our position has worsened for over 20 years straight. CIP is a comprehensive index measuring nations’ ability to produce and export manufactured goods competitively. Technological capability, industrial diversity, and export sophistication can be inferred by this index. Unsurprisingly, CIP closely followed the trend in business investment in research and development during the same period (Chart 1).

Figure 1: Canada’s position in competitive industrial performance has been worsening in parallel to declining business expenditure on R&D

Canada has underperformed G7 in patenting over the last 10 years. During the 30-year period, Canada increased its patent rate 3-fold, while G7 increased its patent rate 5-fold (Chart 2). Canada’s patent performance ranks near the very bottom, just above Italy. This is not simply due to a slower population growth in Canada relative to G7 or the world. Canada’s share of the world population has been stable at approximately 0.5% while its share of world patents declined to 0.9% from 2.3% over the last 30 years. We essentially became a less inventive country with huge implications for productivity and standard of living.

Figure 2: Canada’s performance in patent cooperation treaty (PCT) publications lagging its peers for two decades

Source: World Intellectual Property Organization (WIPO); Conference Board of Canada

Paired with Canada’s low business R&D spending, we can see its struggle to conduct and commercialize innovative research. Improving Canada’s performance in patenting will start with improving business R&D and collaborations with post-secondary institutions to move research into innovative products and services.

Patenting is also crucial for scaling Canadian firms into international competitors because intellectual property determines their ability to protect and “charge rents” for their ideas. IP also allows firms the “freedom to operate” in their field of use. An approach to develop competitive IP strategies is to identify where Canada has sectoral specialization and strength and support those areas. However, the lack of evidence-based guidance for technology-specific innovation policy. The lack of systematic evidence regarding Canada’s specialization and competitiveness in respective technology fields prevents us from evaluating whether current policies are supporting the set of sectors that would maximize the impact of public policy. Supporting sectors that display comparative advantages makes economic sense because those sectors signal that they have already passed a “market test” and further support would accelerate the accumulation of physical and human capital.

Developing such a systematic understanding will provide a strong foundation for prioritizing technology fields for public policy support (Narassimhan et al., 2024). Patent performance is associated with innovation (OECD, 2023) which in turn drives long-run economic growth (OECD, 2010) There is a need for taking a sectoral approach to innovation policy because: 1) the complexity of modern economies requiring horizontal policies to be supplemented by more targeted interventions (sector-specific obstacles to growth), 2) Certain sectors or technologies hold a significant influence on the overall economy, emphasizing the need for focused attention and support due to their outsized importance (Balawejder and Ellys Monahan).

We could develop such crucial baseline knowledge by applying a dual analytical approach comprised of location quotient (LQ) with shift-share analysis (SSA) to patent data.

Findings from the LQ analysis will allow us to assess current policy support for certain technology areas as well as recommending new technology areas for public support. First, consistent strong specialization (as measured by LQ), in specific technology fields indicates that there are domestic factors or sectoral compositions that support Canada’s businesses and research institutions in those technology fields. This finding allows us to systematically assess whether there is an overlap between the technology fields in which Canada (and its regions) is specialized and those technologies that Canadian government considers as priority.

On the other hand, findings from SSA will provide insights into where public policies or interventions could have the most impact by identifying technology fields where the nation has a competitive edge or lags the global average. Ascertaining technology fields (if any) where national component of growth is positive for Canada (or its regions) could be interpreted as indicative of national/regional competitive advantage, thus providing support for continued policy support for those technologies. Conversely, technology fields where the national component of growth is negative for Canada (or its regions) could be interpreted as indicative of the lack of national/regional competitive advantage, thus policy support for those industries has less leverage and likely less predicted impact.

Advanced technologies are key to solving Canada’s low labor productivity and industrial competitiveness problems (Statistics Canada). We can lead the world in the development and applications of those technologies only if our public policies and other support mechanisms are developed on the basis of our existing strengths. Technological prioritization is key to ensuring long-term success of our science and technology strategies and improving Canada’s innovation performance.

1 The average of the following 18 indicators and indices. Manufacturing value-added per capita; manufactured exports per capita; impact of a country on world manufactures trade; impact of a country on world MVA; medium and high-tech manufacturing value-added (MVA) share in total MVA; medium and high-tech manufactured exports share in total manufactured exports; manufacturing value-added share in total GDP; manufactured exports share in total exports; share of world manufacturing exports index; share of medium and high-tech activities in manufacturing export index; manufactured exports per capita index, industrial export quality index; share of manufactured exports in total exports index; share of world MVA index; industrialization intensity index; share of medium and high-tech activities in total MVA index; MVA per capita index; share of MVA in GDP index.

2 The same trend is observable in compounded annual growth rates (CAGR). Canada registered 3.7% annual average growth rate while G7 did 5.7% over that period.

3 Horizontal policies include infrastructure provision, education and skills policy, general innovation subsidies.

4 LQ measures the concentration of a particular technological or industrial activity in a region or a country compared to its concentration at a higher geographical level (world).

5 SSA decomposes the national growth into three components (global effect, industry mix, competitive shift) by comparing national growth to a broader benchmark, typically a global average.